Life doesn’t always turn out as we’d hoped or planned. Almost 100 children suffer the loss of a parent every day in Britain. There are nearly 160,000 deaths from heart disease each year in the UK – an average of 435 people each day. In 2016, there were more than 163,000 deaths from cancer.

Tailored policies

Policies can pay out lump sums or provide an income to ease the financial burden at a difficult time. Cover can be arranged to suit your age and lifestyle, for a term that meets your family’s needs. Cover can be combined to include, for example, critical illness insurance and death benefits within the same policy.

More concern over health issues

It seems that the message that it’s important to have the right type of protection policy in place is increasingly being listened to. In the first six months of this year, financial software company IRESS, recognised a positive trend in the sale of protection products. There was an overall increase of 35.1% in the take-up of term life insurance and income protection policies, through their software1, compared with the first half of 2017.

Insurers believe that this rise is due in part to greater health consciousness, and a better understanding of the part that protection policies can play in keeping a roof over a family’s head, ensuring that household bills can still be paid if death or illness were to strike. If you’d like advice on choosing the right insurance cover for your needs, do get in touch.

A new survey from a major insurer shows that 14% of people think they will still be paying their mortgage at age 701.

Not so long ago, mortgages were likely to be for 25 years, and homebuyers would often be aged in their 20s when they took them out. However, times have changed. Many people are getting on the housing ladder later and house prices are higher. This has led to lenders regularly granting mortgages for much longer terms. This means that one in seven people could expect to be repaying their mortgage into what would normally be considered their retirement years.

If this trend continues, many people will need to factor mortgage repayments into their retirement planning and may even have to consider working past their normal retirement date to cover the cost. Whilst some may wish to stay active in the workplace for longer, not everyone will want to face this prospect.

If you’d like to consider your mortgage options as part of your retirement planning, do get in touch.

1 Aegon, 2018

Your home or property may be repossessed if you do not keep up repayments on your mortgage.

As of 9 January, companies that make unsolicited phone calls to people about their pensions will be liable to enforcement action, including fines of up to £500,000.

The ban has been introduced in a bid to prevent people falling victim to cold call scams that can lead to them losing their life savings. As many as eight scam calls take place every second – or a whopping 250 million calls a year – according to research from the Money Advice Service (MAS).

Reports made to Action Fraud show how highly sophisticated fraudsters have tricked people into transferring their pensions into fraudulent schemes. Victims of pension scams can lose their life savings, and be left facing retirement with limited income. According to the Financial Conduct Authority, pension fraudsters stole on average £91,000 per victim in 2018.

The ban prohibits cold-calling in relation to pensions, except where:

the caller is authorised by the FCA, or is the trustee or manager of an occupational or personal pension scheme, and

the recipient of the call consents to calls, or has an existing relationship with the caller.

Cold calling is currently by far the most common method used to initiate pension fraud. Other scam tactics include:

Unexpected contact about your pension via post or email.

Promises of guaranteed high returns and downplaying the risks.

Offering unusual or overseas investments that aren’t regulated by the FCA e.g. overseas hotels, forestry, green energy schemes.

Putting people under pressure to make a quick decision, for example with time-limited offers, and sending a courier round with paperwork to sign.

Claiming to be able to unlock money from an individual’s pension (which is normally only possible from age 55).

The FCA and TPR are urging the public to be ScamSmart with their pension and always check who they’re dealing with.

The HM Treasury offers the following advice:

If you receive a cold call about your pension, get any information you can, such as the company name or phone number, and report it to the Information Commissioner’s Office via their website or on 0303 123 1113.

If you have been affected by this, or any other scam, report it to Action Fraud by calling 0300 123 2040, or by using the online reporting tool at www.actionfraud.police.uk

By clicking on one of these links you are departing from the regulatory site of Polestar. Neither Polestar nor Positive Solutions is responsible for the accuracy of the information contained within the linked site.

The world’s share markets mostly saw falls in 2018.

2018 was a very different year for investors from 2017. During that year, the share markets generally produced positive returns with very little volatility. Both years had their fair share of dramas, with Brexit and Donald Trump sources of concern across the 24 months. However, whereas in 2017 stock markets seemed relatively unphased by events, the opposite was true in 2018.

In sterling terms, the MSCI World Index was down 4.9%, much less than the main UK indices. However, this hides two factors:

The US stockmarket, which forms about half of the World Index, was relatively strong. Strip that out and the MSCI World Index ex-USA was down 11.2% in sterling terms, only marginally less than the main UK indices.

The Brexit-battered pound was weak during 2018, which flattered overseas returns.

In the UK, the main indices produced their worst annual return since the financial crisis year of 2008. As a result, the UK stock market now has an average dividend yield of nearly 4.5%, the highest level since 2009.

If you are investing for income that yield is undoubtedly attractive. We’re always here to discuss your portfolio and options – and 2019 is going to be an interesting year.

The value of your investment can go down as well as up and you may not get back the full amount you invested. Past performance is not a reliable indicator of future performance. Investing in shares should be regarded as a long-term investment and should fit in with your overall attitude to risk and financial circumstances.

When financial markets are volatile, you often hear that “uncertainty” is the cause. This suggests that uncertainty comes and goes, but because financial markets are forward looking, and because the future is unpredictable, investors must cope with uncertainty all the time.

That can be hard, especially in volatile periods when the value of your investments is fluctuating from day to day. How can investors learn to cope with pervasive uncertainty?

Pricing-in uncertainty

It is important to remember that the market is a very effective information processing machine. This means that millions of market participants around the world are continually assessing information and its expected effect on future cash flows and that prices change as participants act on this. It is therefore reasonable for you to work on the assumption that today’s market level has priced in current uncertainty.

Benefits of hindsight

Investors can also take comfort from remembering that a globally-diversified portfolio has recovered from many periods of uncertainty and crisis.

For example, in 2008 the stock market dropped in value by almost half. It was a period of uncertainty so acute that the viability of global money markets as we know them came into question. Headlines such as “Worst Crisis Since ’30s, With No End Yet in Sight,” “Markets in Disarray as Lending Locks Up,” and “For Stocks, Worst Single-Day Drop in Two Decades” were elevated from the business page to the front page.

Every political or economic crisis poses different challenges and affects the market in different ways, but the experience of past events can help investors maintain perspective.

The temptation to react to events can be strong but reacting is not always the best thing to do. In the heat of the moment in the financial crisis, some people decided to sell out of stocks. Those that stayed the course and stuck to their approach have long since recovered from the crisis and benefited from the subsequent rebound in markets.

There have been many periods of substantial volatility in the past. Exhibit 1 (page 3) helps illustrate this point. The exhibit shows the simulated performance of a balanced investment strategy following several crises, including the bankruptcy of Lehman Brothers in September of 2008, which took place in the middle of the financial crisis. Each event is labeled with the month and year that it occurred or peaked.

Although a globally diversified balanced investment strategy invested at the time of each event would have suffered losses immediately following most of these events, financial markets did recover, as can be seen by the three-, five- and ten-year cumulative returns shown in the exhibit. In advance of such periods of discomfort, having a long-term perspective, appropriate diversification, and an asset allocation that aligns with their risk tolerance and goals can help investors remain disciplined enough to ride out the storm. A financial adviser can play a critical role in helping to work through these issues and in counseling investors when things look their darkest.

Conclusion

As we know, predicting future events correctly, or how the market will react to future events, is difficult. The good news is that being a successful investor does not rely on making accurate predictions. It is important to understand that market volatility is a part of investing and to enjoy the benefit of higher potential returns, investors must be willing to accept increased uncertainty. Accurately predicting the future is not a prerequisite to be a successful investor.

A key part of a good long-term investment experience is being able to stay with your investment philosophy, even during tough times. A well‑thought‑out, transparent investment approach can help people be better prepared to face uncertainty and may improve their ability to stick with their plan and ultimately capture the long-term returns of capital markets.

Markets Rewarding Discipline

Jake DeKinder, Head of Advisor Communication at Dimensional Fund Advisors Ltd, explains how capital markets have rewarded investors who are able to tune out short-term noise and stay disciplined over the long term.

Balanced Strategy 60/40: The model’s performance does not reflect advisory fees or other expenses associated with the management of an actual portfolio. There are limitations inherent in model allocations. In particular, model performance may not reflect the impact that economic and market factors may have had on the adviser’s decision making if the adviser were actually managing client money. The balanced strategies are not recommendations for an actual allocation.

Dimensional All Country World Core 2 Index: Compiled by Dimensional from Bloomberg securities data. The index targets all the securities in the eligible markets with an emphasis on companies with smaller capitalisation, lower relative price, and higher profitability. Profitability is measured as operating income before depreciation and amortisation minus interest expense scaled by book. Exclusions: REITs and investment companies. The index has been retroactively calculated by Dimensional Fund Advisors and did not exist prior to April 2008. The calculation methodology was amended in January 2014 to include profitability as a factor in selecting securities for inclusion in the index.

The Dimensional and Fama/French Indices reflected above are not “financial indices” for the purpose of the EU Markets in Financial Instruments Directive (MiFID). Rather, they represent academic concepts that may be relevant or informative about portfolio construction and are not available for direct investment or for use as a benchmark. Their performance does not reflect the expenses associated with the management of an actual portfolio. Index returns are not representative of actual portfolios and do not reflect costs and fees associated with an actual investment. Actual returns may be lower. See the appendix for descriptions of the Dimensional and Fama/French indexes.

The Dimensional Indices have been retrospectively calculated by an affiliate of Dimensional Fund Advisors Ltd. and did not exist prior to their index inceptions dates. Accordingly, results shown during the periods prior to each Index’s index inception date do not represent actual returns of the Index. Other periods selected may have different results, including losses. Backtested index performance is hypothetical and is provided for informational purposes only to indicate historical performance had the index been calculated over the relevant time periods. Backtested performance results assume the reinvestment of dividends and capital gains.

Source: Dimensional Fund Advisors Ltd.

The views and opinions expressed in this article are those of the author and not necessarily those of Dimensional Fund Advisors Ltd. (DFAL). DFAL accepts no liability over the content or arising from use of this material. The information in this material is provided for background information only. It does not constitute investment advice, recommendation or an offer of any services or products for sale and is not intended to provide a sufficient basis on which to make an investment decision.

RISKS

Investments involve risks. The investment return and principal value of an investment may fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original value. Past performance is not a guarantee of future results. There is no guarantee strategies will be successful. Diversification neither assures a profit nor guarantees against loss in a declining market.

Jake DeKinder, Head of Advisor Communication at Dimensional Fund Advisors Ltd, explains how capital markets have rewarded investors that are able to tune out short-term noise and stay disciplined over the long-term.

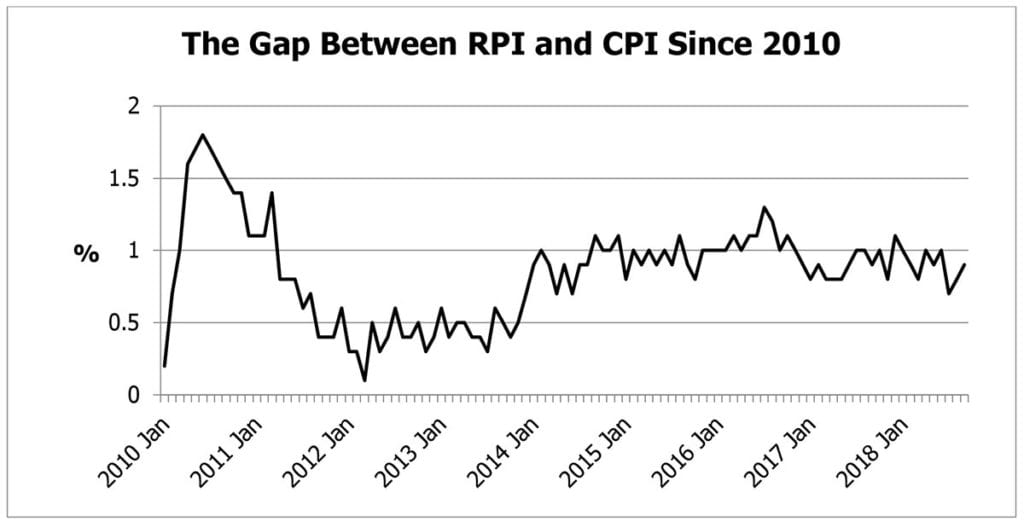

The popular National Savings & Investments (NS&I) savings certificates will be indexed to CPI instead of RPI from next year.

The certificates have not been on sale since 2011, but NS&I allow existing certificate holders to reinvest in new series of certificates when their old ones mature. The terms have gradually worsened over the years and at present reinvestment promises a return of RPI inflation +0.01% a year. For certificates maturing from 1 May 2019, the basis of indexation will change from RPI to CPI.

The change was not picked up by newspapers at the time because they were released the Friday before the 2018 Budget, held on the Monday. Government departments are often accused of burying bad news, and the downgrading of the NS&I index-linked savings certificates is certainly bad news for affected investors.

RPI or CPI?

The government now generally only uses RPI where it benefits, for example as the basis for interest levied on student loans or for annual rail fare increases. CPI is used to index many – but not all – income tax bands and allowances.

NS&I said, ‘This change recognises the reduced use of RPI by successive governments and is in line with NS&I’s need to balance the interests of its savers, the cost to the taxpayer, and the stability of the broader financial services sector.’

As the graph shows, the move from RPI to CPI will cut returns by about 0.8% a year based on data since 2010. In their widely-missed press release, NS&I note that, ‘The cost to the taxpayer is forecast to reduce by £610 million over the next five years’. That ‘cost to the taxpayer’ could also be read as, ‘return to the investors’.

If you hold any issues of index-linked certificates, think about whether you definitely want to reinvest when they next mature, rather than letting inertia (and automatic reinvestment) take its course.

The value of investments and the income they produce can fall as well as rise. You may get back less than you invested.

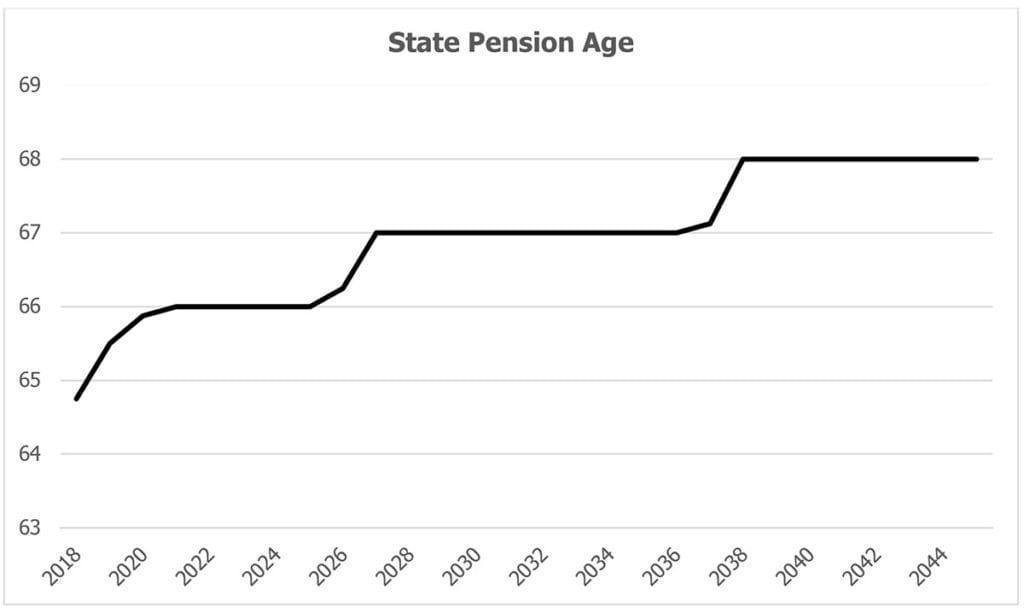

The State Pension Age (SPA) became equal for men and women for the first time, at age 65, on 6 November 2018.

Having reached this landmark, the next stage of SPA increases has already started. For both men and women, the state pension will become payable for anyone born between 6 December 1953 and 5 January 1954 on 6 March 2019. The SPA will then be increased to reach age 66 by October 2020.

The SPA is scheduled to rise again as existing legislation already covers the increase from 66 to 67, phased in over two years from April 2026. The same legislation provides for a step up to 68, starting in April 2044.

However, in July 2017 the Department for Work and Pensions announced it would accept the recommendations of the Cridland Review – this brings the start of the move to a SPA of 68 forward to April 2037. Legislation for this change has been deferred until after the next SPA review in 2023 – raising the SPA in the current political conditions could prove difficult for the government – but if your SPA will be at least 68 if you were born after 5 April 1971.

Rising life expectancies

The rising SPA is linked to historic improvements in mortality – in effect they match the increases in life expectancy at age 65 of 8 years for men and 9 years for women since the early 1950s.

The Cridland Review has anticipated future increases in life expectancy as an argument for accelerating the increase in SPA. However, data from the Office for National Statistics issued in September, suggest that increases in life expectancy may have come to an end, at least for the time being.

The arrival of the equalised SPA provoked a fresh round of protests from women born in the 1950s, who started working life with an expectation that their state pension would be payable from age 60. The government has previously made a minor concession on the phasing of the change but further offers are not expected. The simple reason is cost: a higher SPA reduces government pension expenditure and raises extra National Insurance Contribution revenue.

If you want to retire when you choose, rather than the State decides, make sure your private pension provision is adequate.

The value of your investment can go down as well as up and you may not get back the full amount you invested.

Past performance is not a reliable indicator of future performance.

The government has revived plans to raise probate fees in England and Wales.

A new, banded structure for probate fees in England and Wales is to be introduced, according to a written statement issued a week after the 2018 Budget by the Parliamentary Under Secretary of State for Justice.

The announcement comes after the absence of inheritance tax (IHT) reforms in the Budget, despite the Chancellor commissioning a review by the Office of Tax Simplification in January 2018. The only change to IHT announced in October was a small adjustment to the legislation for the residence nil rate band – this being such a complex piece of legislation, it had been wrongly drafted.

New fee structure

If new probate fees sound familiar, it is because a very similar announcement was made in March 2017. At the time the proposal provoked widespread criticism, because the higher levels were seen to be more of a new tax than a simple fee adjustment. In the event the planned change fell victim to the legislative logjam around the last General Election and disappeared.

Since then, the government has taken on board some of the original criticism and cut the fees they are proposing, particularly for larger estates.

The current fees are £215 for individual applications and £155 via a solicitor, with nothing payable if the estate value is up to £5,000. Under the new banding, there is a maximum effective charge for probate of 0.5% of the estate, which is triggered at £50,000 (a £250 fee) and £500,000 (a £2,500 fee).

The new fees are currently scheduled to come into effect 21 days after the legislation is passed, and there is very little that can be done to mitigate the impact. They are payable even if the estate passes with no IHT liability, as is usually the case on the first death of a married couple or civil partners, or if the value of the estate is covered by the available nil rate and residence nil rate bands.

There are still opportunities to save IHT with careful planning and, as the Budget made no significant changes, there remains a window of opportunity before any reforms are introduced.

If you would like help updating your estate plans ahead of the review publication please get in touch.

Value of estate

Old

Proposal

New

Legislation

Up to £50,000 or exempt from requiring a grant of probate

Nil

Nil

£50,001 – £300,000

£300

£250

£300,001 – £500,000

£1,000

£750

£500,001 – £1,000,000

£4,000

£2,500

£1,000,000 – £1,600,000

£8,000

£4,000

£1,600,001 – £2,000,000

£12,000

£5,000

Over £2,000,000

£20,000

£6,000

The value of tax reliefs depends on your individual circumstances.

Tax laws can change.

The Financial Conduct Authority does not regulate tax or trust advice.

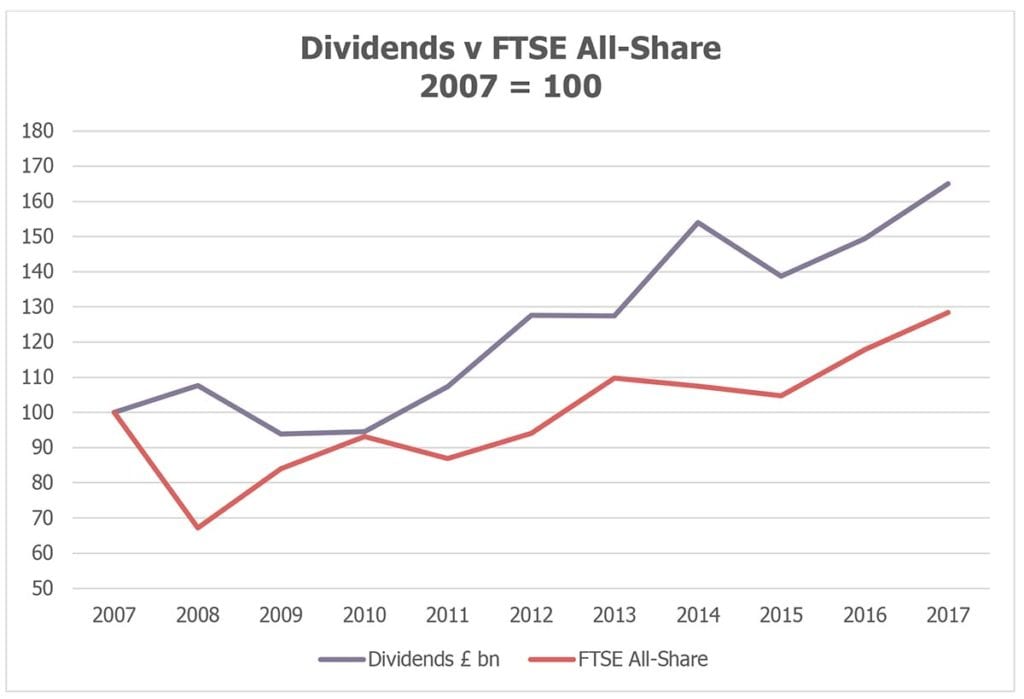

UK dividends are continuing to grow faster than inflation, according to the latest quarterly data from Link Asset Service.

The latest UK Dividend Monitor (UKDM) shows that in the third quarter of 2018 dividend payments were 4.1% up on the previous year, comfortably above the current rate of inflation. Looking over the 10-year period from the end of 2007 to the end of 2017, total dividend payments have risen by an average of 5.1% while CPI inflation has averaged 2.4%.

The UKDM is published by Link Asset Services (formerly produced by Capita) and totals the dividends paid out on the ordinary shares of companies listed on the UK Main Market every quarter – excluding investment companies, to avoid double counting. It captures both regular dividends and one-off special dividends, which often stem from takeovers or other corporate restructurings.

As the graph shows, over the last ten years, the amount paid out in dividends has grown faster than the capital value of shares. There are still dips, but between 2007 and 2017 the regular dividend total dropped only once, in the wake of the global financial crisis. The jump and dive between 2013 and 2015 is an aberration caused by a one-off £15.9 billion special dividend paid by Vodafone in 2014.

Unpredictable markets

Despite increasing dividend payments, there has been considerable volatility in UK share prices throughout 2018. Little more than five months, and over 1,000 points, separate the FTSE 100’s high and low marks for the year to date. But whilst the FTSE tracks capital values, it does not account for dividends, which are ignored in the calculations of most equity market indices.

If you are investing for income the data is a reminder that, for all the fluctuations in capital values, shares have continued to provide real dividend growth.

The value of your investment can go down as well as up and you may not get back the full amount you invested.

Past performance is not a reliable indicator of future performance.

Investing in shares should be regarded as a long-term investment and should fit in with your overall attitude to risk and financial circumstances.