The Chancellor has changed his mind – again – on National Insurance Contributions (NICs) for the self-employed. The Treasury has revealed that Class 2 NICs will remain for at least the rest of this Parliament.

The Treasury’s justification was that, without Class 2 NICs, “A significant number of self-employed individuals on the lowest profits would have seen the voluntary payment they make to maintain access to the state pension rise substantially.”

This means that over three million people will continue to pay the tax, providing more revenue for the Chancellor at a time that he certainly needs it. However, as many as 300,000 self-employed people earning less than the Small Profits Threshold (£6,032 a year) could have seen their NIC payments rise from £2.95 a week to £14.65 a week.

Mr Hammond originally proposed a reform of National Insurance Contributions (NICs) for the self-employed in his March 2017 Budget. The 2017 proposal was to increase the main rate of Class 4, from 9% to 10% in 2018/19 and again to 11% in 2019/20, bringing it closer to the employee rate of 12%.

The idea lasted less than a week before it was buried under a welter of backbench criticism and The Sun newspaper’s campaign. Some months later, the Treasury quietly announced that the end of Class 2 NICs would be deferred a year. Now they could survive until 2022, based on the current deadline for the next General Election.

The decision, announced well ahead of the Budget in October, is a reminder of the financial and political constraints faced by the Chancellor. It should also jog your memory about pre-Budget planning – the Chancellor does not appear to be in a position to give anything away.

The value of tax reliefs depends on your individual circumstances.

Tax laws can change.

The Financial Conduct Authority does not regulate tax advice.

A leading think tank has proposed a radical shake up of the UK tax system.

The Institute for Public Policy Research (IPPR) is a centre-left think tank that has a long history of influencing Labour Party policy. So, its ideas on tax reform published in the final report of its ‘Commission on Economic Justice’ are of more than just academic interest.

Income tax and national insurance

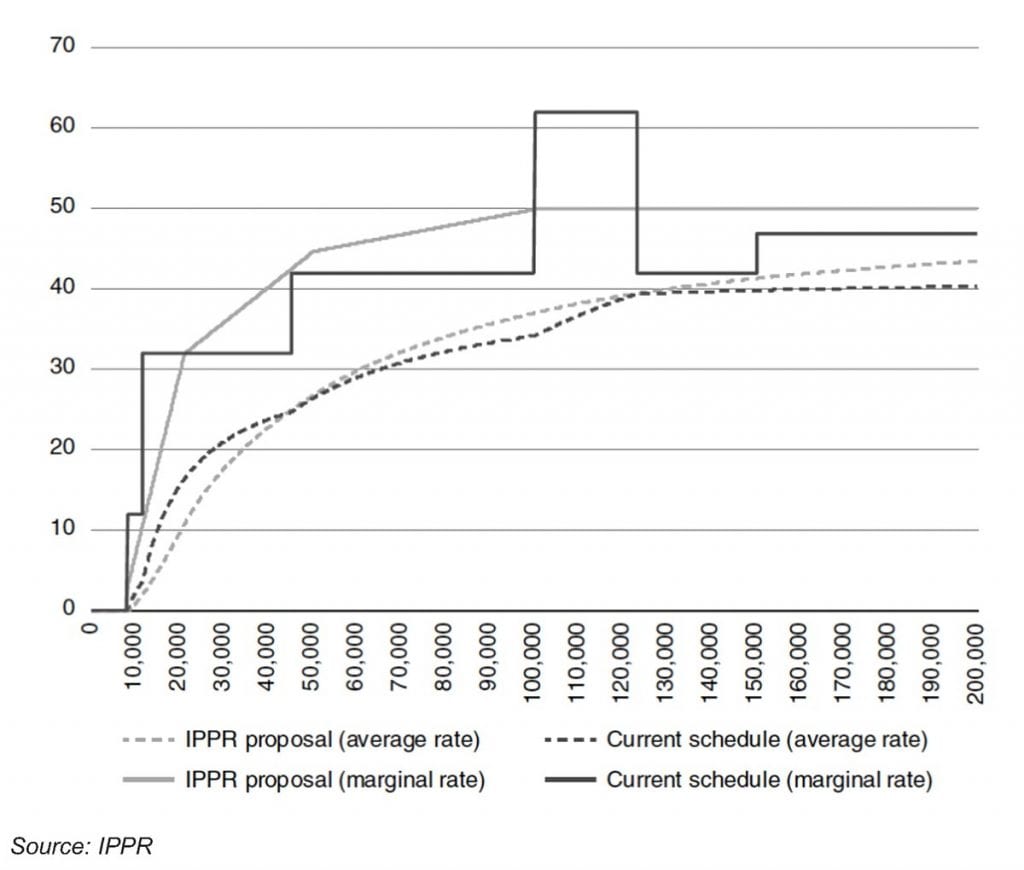

The IPPR propose combining income tax and national insurance contributions (NICs) into a single tax, applicable to all income, including investment income. They would replace the current system of incremental tax bands with a gradually rising rate applied to all taxable income, capped at a maximum 50% marginal rate above £100,000. Their proposal would smooth out inconsistent marginal rates, as the graph shows.

Inheritance tax (IHT)

The IPPR supports the recent proposals from the Resolution Foundation to abolish IHT. The IPPR would replace IHT with a lifetime gifts tax, payable by the recipient of a gift or legacy (other than a spouse or civil partner) – currently IHT is usually paid by the estate. Income tax rates would apply once a lifetime receipts allowance of £125,000 has been reached. According to the IPPR, this tax structure would raise much more than IHT, as it would largely remove the benefit of making gifts during lifetime.

Capital gains tax

The IPPR propose abolishing “most exemptions”, other than for the main residence. Capital gains would instead be taxed at income tax rates, implying a maximum marginal rate of 50% under their proposed income tax structure. Taxing capital gains as income is not a new idea – it was a practice previously introduced in the late 1980s, by the Conservative Chancellor, Nigel Lawson.

Corporation tax

Instead of cutting the corporation tax rate from 19% to 17% in 2020, the IPPR proposes increasing the rate to 24%, with business reliefs and allowances ‘simplified’ (i.e. cut back) to broaden the tax base. To tackle multinational tax avoidance (a practice associated with the FAANS companies, Facebook, Apple, Amazon, Netflix and Google), the IPPR proposes an alternative minimum corporation tax, pro-rating global profits to the proportion of global turnover in the UK.

These wide-reaching proposals are unlikely to be implemented exactly as the report proposes. But if we do see a Labour government, the IPPR could become more relevant, quite quickly.

The value of tax reliefs depends on your individual circumstances.

Tax laws can change.

The Financial Conduct Authority does not regulate tax advice.

The 2018 Budget has been set for Monday 29 October, setting a deadline for speculation and proposals. Mr Hammond, however, has indicated that he won’t end the long spell of austerity measures, despite improving public finances.

Proposals raised by think tanks and professional bodies include overhauls of income and inheritance tax, ‘pension tax relief simplification’, and scrapping entrepreneur’s relief to help fund NHS costs.

But every proposal is overshadowed by Brexit, and the uncertainty of what will happen on 29 March 2019.

What’s coming?

Alongside measures announced in the draft Finance Bill, the following areas could see change:

The NHS

The NHS Foundations’s ten-year plan may not be published in time for the Budget, so the Chancellor could be limited to general spending priorities. Mr Hammond said a digital services tax or ‘Google tax’ is coming – with or without European allies. This income could be dedicated to the NHS.

Inheritance tax (IHT)

The IHT review from the Office of Tax Simplification (OTS) may be published ahead of the Budget. It was tasked to look at making IHT less complex, focusing especially on trusts, administrative issues and business and agricultural property reliefs. Calls for a complete overhaul in favour of a ‘lifetime receipts’, ‘property’ or ‘wealth tax’ seem unlikely from a Conservative government.

Stamp duty

After introducing new reliefs for first-time buyers, focus has shifted to ‘last time’ buyers, with calls to incentivise older homeowners to downsize. The Prime Minister has also indicated that an additional 1-3% duty could be levied on foreign property buyers to help control rising house prices and tackle homelessness.

Business

Business rates are due to increase next year, with business groups calling for action. The Chancellor’s conference speech outlined changes to the apprenticeship levy to help build training and skills for SMEs, and appeared to boost commitment to the business sector.

The environment

We are likely to see a dedicated plastics packaging tax. Initial reports indicated the costs would be borne by manufacturers rather than consumers. However, we may also see an increase to the plastic bag levy from 5p to 10p and roll out to all shops, not just firms with over 250 employees.

In this most turbulent of times, facing pressure from many groups, perhaps the only clear thing is that Mr Hammond has an unusually tricky balancing act to pull off.

Action Fraud launches a campaign to warn people about the threat of Computer Software Service fraud, one of the country’s most reported top five frauds.

What is Computer Software Service Fraud?

Computer Software Service fraud can start with either a phone call, an email or a pop-up message appearing on your computer, stating there is something wrong with your computer or internet connection and that it needs to be fixed. However, there will either be a demand for payment to fix it, or they will install software on the computer which will allow the criminals to access personal and financial details.

New intelligence

In 2017/18, Action Fraud received 22,609 reports of Computer Software Service fraud with a total of £21,365,360 being lost to fraudsters. An intelligence report run by the City of London Police’s National Fraud Intelligence Bureau has shown that men and women are equally susceptible to being targeted and the average age of a victim is 63. Figures also show that those living in London and Bristol are most likely to fall victim.

How to protect yourself from Computer Software Service fraud

Computer firms do not make unsolicited phone calls to help you fix your computer. Fraudsters make these phone calls to try to steal from you and damage your computer with malware. Treat all unsolicited phone calls with scepticism and don’t give out any personal information.

Computer firms tend not to send out unsolicited communication about security updates, although they do send security software updates. If in doubt, don’t open

the email.

Computer firms do not request credit card information to validate copies of software. Nor do they ask for any personally identifying information, including credit card details.

If you have been affected by this, or any other scam, report it to Action Fraud by calling 0300 123 2040, or by using the online reporting tool at www.actionfraud.police.uk

By clicking on one of these links you are departing from the regulatory site of Polestar. Neither Polestar nor Positive Solutions is responsible for the accuracy of the information contained within the linked site.

Readers of this note could be forgiven for thinking that the world in general, and the UK specifically, is in a right old state. There’s certainly lots to be thinking about – Trump’s belligerence, China’s debt mountain, Putin’s malevolence, not forgetting Brexit and the prospect of a far-left leaning Labour Government. This inevitably leads to understandable concern for what this all means for investment portfolios. This note seeks to reassure the reader that well-structured portfolios are capable of riding out any storm.

What a mess

It is rare that politics is discussed in our articles about investing, but it is evident when turning on the news that it feels like there is much going on in global politics at the moment that is unsettling, complex and confusing at one end, such as Brexit, to the downright worrying and unpleasant at the other, such as Russian meddling in the democratic process and the use of nerve agents on the streets of Salisbury. There is much in between that is hard to compute in terms of its impact. Trump’s populism feels unpleasant to many, but is his call to NATO members, such as Germany, to meet their commitments in full to share more of the financial burden of protecting Europe unfair, given Russian aggression? Is his trade war with China wholly a bad thing? A recent leader in The Economist[1] supports – at least in part – his tirade against its mercantilism and unfair trade practices. Let’s not forget climate change…

Issues closer to home such as Brexit and the potential for great political uncertainty in the event of no satisfactory (or any) deal being reached, feel – at least to UK residents – more prominent in our lives at this moment than some of these wider issues.

The Brexit affair

Whichever way one voted, it is hard not to be dismayed by the shambles that is Brexit, concocted by all sides. Until recently, the UK appeared to have no clearly defined strategy. Its negotiations are led by a PM who wanted to remain, receiving criticism from the right wing of her party for not going far enough, and daily criticism from the opposition party, led by a long-time Eurosceptic, that still has no credible alternative aside from six ‘cake-and-eat-it’ criteria that any deal must meet. For example, Criteria 2 poses the question ‘Does it deliver the “exact same benefits” as we currently have as members of the Single Market and Customs Union?[2]’, which is an impossibility, unless the deal is to remain. What a mess! One would laugh if the consequences for our nation were not so great.

The EU has hardly covered itself in glory either with their intransigence and deep-seated, implicit desire to make everything so tough that other EU member states won’t dare to follow suit, or that UK voters might change their minds. Yanis Varoufakis – the Greek finance minister at the time of their debt crisis – revealed the trap that the EU would set for the UK government, in his book[3] about his own experiences of dealing with it. Did any of our politicians read it?

In the event that any deal agreed gets voted down in Parliament – or there is no deal – we face a high chance that the Conservative government could fall (but will turkeys vote for Christmas?) to be replaced by a far-left leaning government led by Corbyn and McDonnell. Whatever your own thoughts and preferences on that, the one certainty is that we would be in for a period of radical change. Certainly that means higher personal taxation. In Labour’s 2017 manifesto they gave us a clue: a 45% income tax rate to kick in at £80,000 of income, with a 50% rate above £123,000. This results in marginal tax rates – taking into account National Insurance and tapering of allowances – of 55% for those earning between £80,000 to £100,000, 73% up to £123,000 and 58% thereafter, according to the Institute for Fiscal Studies. Even before these changes it is interesting to note that 4 in 10 adults currently pay no income tax and the top 10% of income tax payers pay 60% of all income tax[4] and around 30% of all personal taxes collected. Corporation tax is set to rise from 19% to 26% and the 10% shareholding held for employees – announced by McDonnell at the Labour Party Conference – is likely to be a large new tax on companies, given the £500 limit per employee on dividend income and with the remainder going to HMRC. Renationalisation of some industries, possibly without full compensation, is not beyond the realms of possibility. Wherever you sit in terms of the balance between equity (how the economic pie is sliced up) and efficiency (how big the pie is), there is no doubt that we are living in ‘interesting’ times.

The point of this note is to recognise that the world we live in can be an uncertain and uncomfortable place and it can create anxiety over our future wealth and well-being. It also sets the context for why and how a sensibly structured portfolio can provide considerable comfort for longer-term investors, and how we can put the uncomfortable noise of what’s going on in perspective.

It is not all bad, in fact, far from it

A recent study by the OECD[5] projects that global (after inflation) growth will rise by 3.7% in both 2018 and 2019, with major European economies growing by 1% to 2%, including the UK (1.3%). Growth in the US is predicted to be around 3% in 2018 and 2019. In the UK, employment is at a record high and real wage growth (after inflation) has been positive since 2015 and the budget deficit is now around 1% of GDP compared to 10% before the austerity program. Global growth leads to a growth in global earnings, which, when added to dividends paid, equates to the economic return due to equity investors for providing capital. That’s good news.

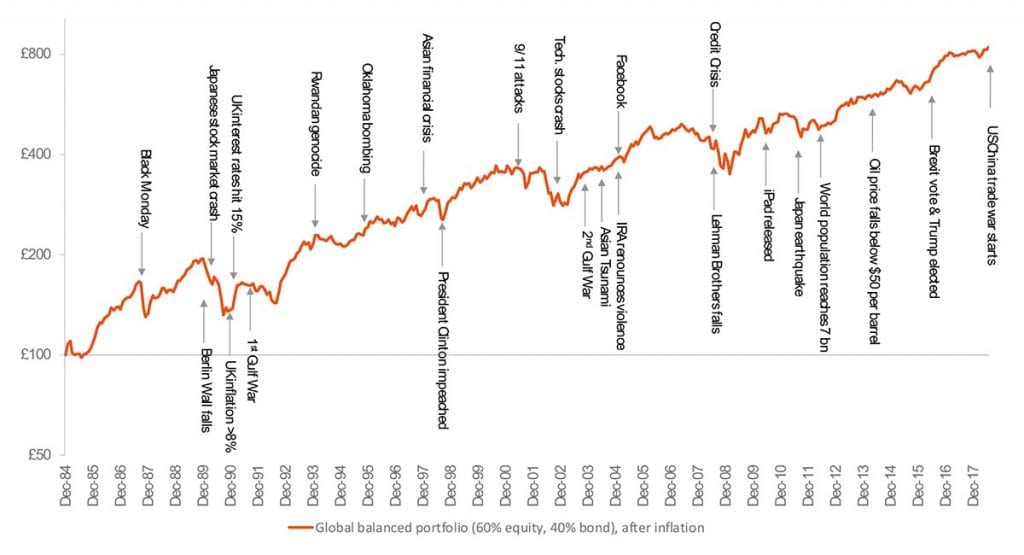

The chart below illustrates that markets weather the multitude of World events they experience, rewarding the patient long-term investor, with growth in their purchasing power.

Figure 1: The relentless growth of purchasing power, despite World events (1/1985-7/2018)

The capitalist spirit continues to drive positive change

Since 2016 alone, 90 million people have been lifted out of extreme poverty[7], something that afflicts 8% (634 million) of the World’s population, most of whom live in Sub-Saharan Africa. South Asia and East Asia and the Pacific have lifted around 0.5 bn and 1 bn people out of extreme poverty, respectively, since 1990[8]. That is on account of the unleashing of the energy and innovation that capitalism has driven in these regions, including China. In terms of infant mortality, the progress has, again, been staggering. In 1990, on a global basis, infant mortality stood at 65 deaths per 1,000 live births. Today it is less than half that at below 30[9]. This is due to the reduction in poverty and improvement in healthcare and education around the globe, again driven and funded by the wealth that capitalism delivers[10].

Please take the time to view an amazing data visualisation of the World’s progress since 1810 by Hans Rosling[11], a renowned global health academic, to lift your spirits (see footnote 8). It’s a great way to spend four minutes.

We, as humans, tend to hold many misperceptions around important issues, overestimating guesses when an issue worries us and underestimating those that do not. In part, this is because we rely on the fast thinking part of our brains, which are often not over-ridden by slower, more measured, reasoning[12]. For example in the UK we guess that 37% of the population is over 65, when in fact it is 17%. We believe that the top 1% of wealthiest people own 59% of the wealth, when in fact it is 23%. Only 13% of the UK’s population are immigrants, yet we guess at 25%[13]. One can begin to see how polarised political system can use facts and misperceptions to their advantage.

So where does all this leave investors and their portfolios?

You may well be asking yourself whether what is going on in the World affects how your money is invested and if any changes need to be made to your portfolio. The question implicitly suggests that we can look into the future and know what is going to happen. If it were that easy, all investors would know what to do and prices would already have moved. Remember that you are not the only person thinking about these global challenges and all scenarios are reflected in current prices. As a consequence, we need to rely on the structure of our portfolios to see us through.

We set out three key risks relating to Brexit and how sensible portfolio structures can mitigate them.

Risk 1: Greater volatility in the UK and possibly other equity markets

In the event of a poorly received deal – or no deal – it is certainly possible that the UK equity market could suffer a market fall as it tries to come to terms with what this means for the UK economy and the impact on the wider global economy. A collapse of the Conservative government and a Labour victory would add further uncertainty.

Risk 2: A fall in Sterling against other currencies

In 2016, after the referendum, Sterling fell against the major currencies including the US dollar and the Euro. There is certainly a risk that Sterling could fall further in the event of a poor/no deal.

Risk 3: A rise in UK bond yields (and thus a fall in bond prices)

The economic impact of a poor/no deal and/or a high spending socialist government could put pressure on the cost of borrowing, with investors in bonds issued by the UK Government (and UK corporations) demanding higher yields on these bonds in compensation for the greater perceived risks. Bond yield rises mean bond price falls, which will take time to recoup through the higher yields on offer.

Looked at in isolation, these may appear to be significant risks. Owning a well-diversified and sensibly constructed portfolio, however, can greatly reduce these risks.

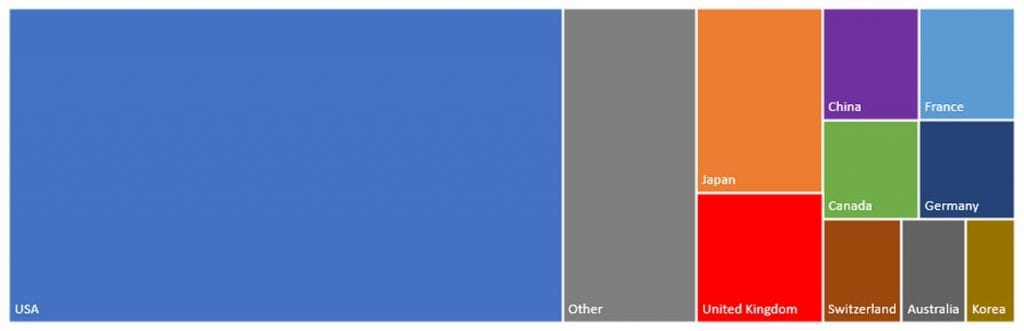

Mitigant 1: Global diversification of equity exposure

Although it is the World’s sixth largest economy (depending on how you measure it), the UK produces 3% to 4% of global GDP, and its equity market is around 6% of global market capitalisation. Many of the companies listed on the London Stock Exchange derive much of their revenue from outside of the UK (around 70% to 80%). For example, HSBC, even though it is often thought of as a British bank, generates over 90% of its revenues from overseas. Well-structured portfolios hold diversified exposure to many markets and companies.

Figure 2: Global market capitalisation (developed and emerging markets) – 2018

Source: Albion Strategic Consulting using data from iShares – August 2018 (MSCI ACWI ETF).

Equity markets are always volatile, responding – sometimes materially – to new information. Despite this, changing your mix between bonds and equities would be ill-advised. Timing when to get in and out of markets is notoriously difficult. Markets move with speed and magnitude and missing out on the best days in the markets can have material long-term return impacts. Provided you do not need the money today, you should hold your nerve and stick with your strategy.

Mitigant 2: Owning non-Sterling assets and currencies in the growth assets

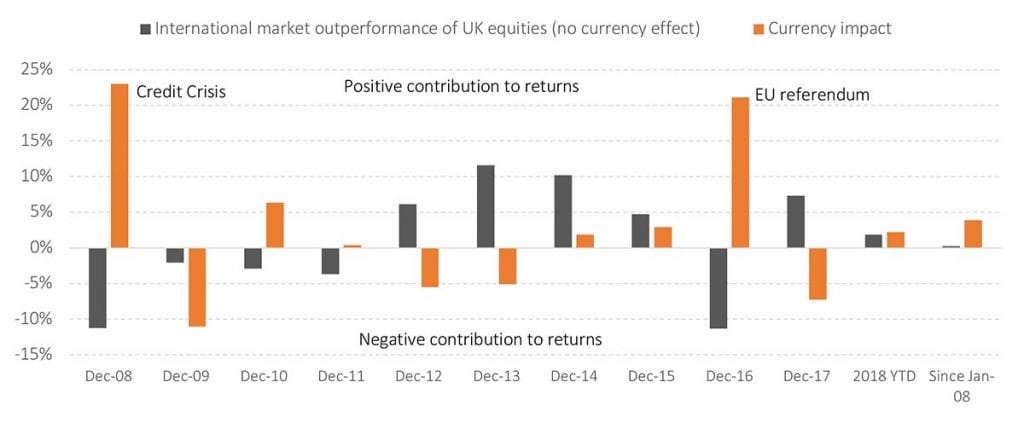

In the event that Sterling is hit hard, it is worth remembering that the overseas equities that you own come with the currency exposure linked to those assets. For example, owning US equities comes with US dollar exposure, as this exposure is not hedged out. In short, a fall in Sterling has a positive effect on non-UK assets that are unhedged. The chart below illustrates the impact that currency in unhedged non-UK assets has had over the past decade. As you can see, at times of market crisis, the Pound has fallen against other safe-haven currencies such as the US dollar.

Figure 3: A falling pound is a positive contributor to portfolio returns

The bond element of your portfolio should have little or no non-Sterling currency exposure to avoid mixing the higher volatility of currency movements with the lower volatility of shorter-dated bonds.

Mitigant 3: Owning short-dated, high quality and globally diversified bonds

Any bonds you own should be predominantly high quality to act as a strong defensive position against falls in equity markets. Avoiding over-exposure to lower quality (e.g. high yield, sub-investment grade) bonds makes sense as they tend to act more like equities at times of economic and equity market crisis. Your bond holdings should be diversified across a number of different global bond markets, which mitigates the risk of a rise in UK yields (and thus falling prices), as the cost of borrowing in other markets may not be impacted in the same way, at the same time.

Some thoughts to leave you with

Even if you cannot avoid watching, hearing or reading the news, it is important to keep things in perspective. The UK is a strong economy with a strong democracy. It will survive Brexit, whatever the short-term consequences that we will have to bear, and so will your portfolio. Keeping faith with both global capitalism and the structure of your portfolio and holding your nerve, accompanied by periodic rebalancing is key. Lean on your adviser if you need support. That is what we are here for.

Perhaps try to catch up on the news only once a week and use the extra time to read about some of the exciting and positive things that are happening in the World.

‘This too shall pass’ as the investment legend Jack Bogle likes to say.

This article is distributed for educational purposes and should not be considered investment advice or an offer of any security for sale. This article contains the opinions of the author but not necessarily the Firm and does not represent a recommendation of any particular security, strategy or investment product. Information contained herein has been obtained from sources believed to be reliable but is not guaranteed.

Past performance is not indicative of future results and no representation is made that the stated results will be replicated.

Errors and omissions excepted.

References

[1] The Economist, September 22nd – 28th edition, ‘Hunker down’, page 12.

[2]www.labourlist.org (2017) Keir Starmer: Labour has six tests for Brexit – if they’re not met we won’t back the final deal in parliament. 27th March 2016.

[3] Yannis Varoufakis (2016), And the weak suffer what they must The Weak Suffer What They Must? Europe’s Crisis and America’s Economic Future, New York: Nation Books, 2016

[12] Nobel Prize winner, Daniel Kahneman’s book ‘Thinking fast and slow’ is a great read on this subject.

[13] Data source: Bobby Duffy (2018), ‘The Perils of Perception: why we are wrong about nearly everything’. Bell & Bain Ltd. Glasgow. A great read on the subject.

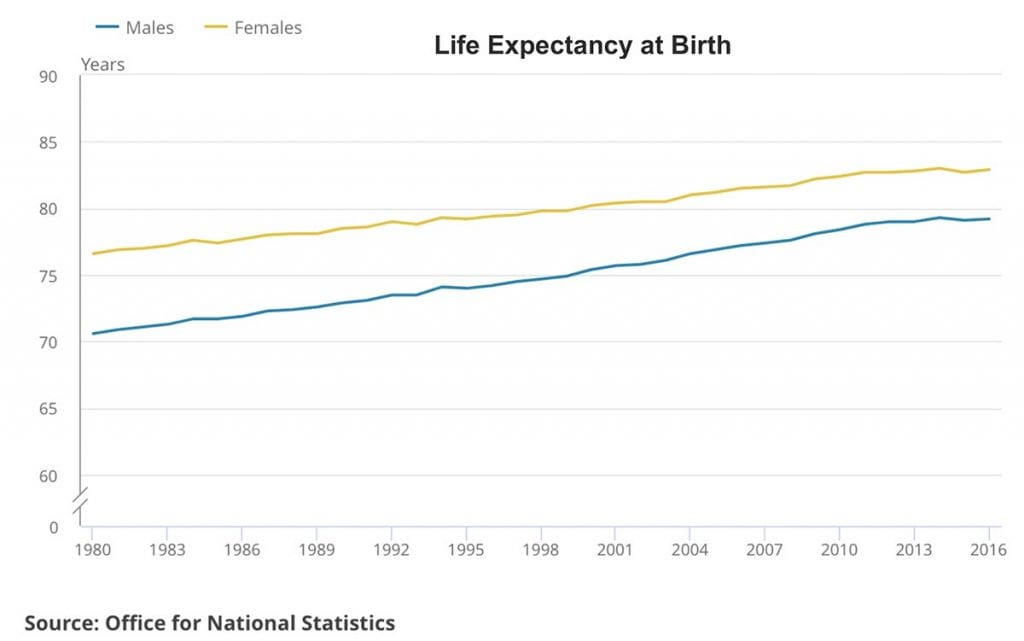

A paper published in August by the Office for National Statistics (ONS) casts new light on life expectancies in the UK.

Life expectancy has been increasing in the UK for a long time, as the graph shows. In 1980, the average life expectancy at birth was 70.6 years for a man and 76.6 years for a woman. In 2016 this had increased to 79.2 years for a man and 82.9 years for a woman.

What the graph also reveals is that the rate of improvement in life expectancy has been slowing down. The ONS data shows a marked deceleration in the 21st century.

Between 2011 to 2016, women’s life expectancy at birth increased by 0.2 years compared with an increase of 1.2 years over the period from 2006 to 2011. For men, the corresponding increases were 0.4 years and 1.6 years. There was a similar effect for life expectancy at age 65, which rose by only 0.1 years for women and 0.3 years for men between 2011 and 2016, against 1 year and 1.1 years in the previous five years.

For the layman, this welter of data can be confusing, especially as the press coverage is not always well informed. A few important things to understand are:

The ONS life expectancy data imply that, on average, a man who was 65 years old in 2012 will live until 83.7, while a woman who was 65 years old in 2012 will survive until 86. The expected age at death also rises with age attained.

The data represents the entire UK, but past research has revealed significant differences between regions and even within the areas of single cities.

As well as regional variation, different sections of the population experience different mortality. For example, those with private pensions tend to live longer, probably because they are wealthier.

Crucially, the life expectancies are averages, so 50% of people will outlive the central figure. The spread around the widely-quoted average is significant and often overlooked. The ONS’s own ‘How long will my pension last’ website (which has not been updated with the new data yet) shows that a 65-year-old man has a one-in-four chance of living until 94, and a woman of the same age a one-in-four chance of living to 96.

The data suggests your retirement may not be quite as long as previously thought, but there is still a good chance you will be living into your 90s. If your pension planning does not reflect that, the sooner you review it, the better.

The value of your investment can go down as well as up and you may not get back the full amount you invested.

Past performance is not a reliable indicator of future performance.

The value of tax reliefs depends on your individual circumstances.

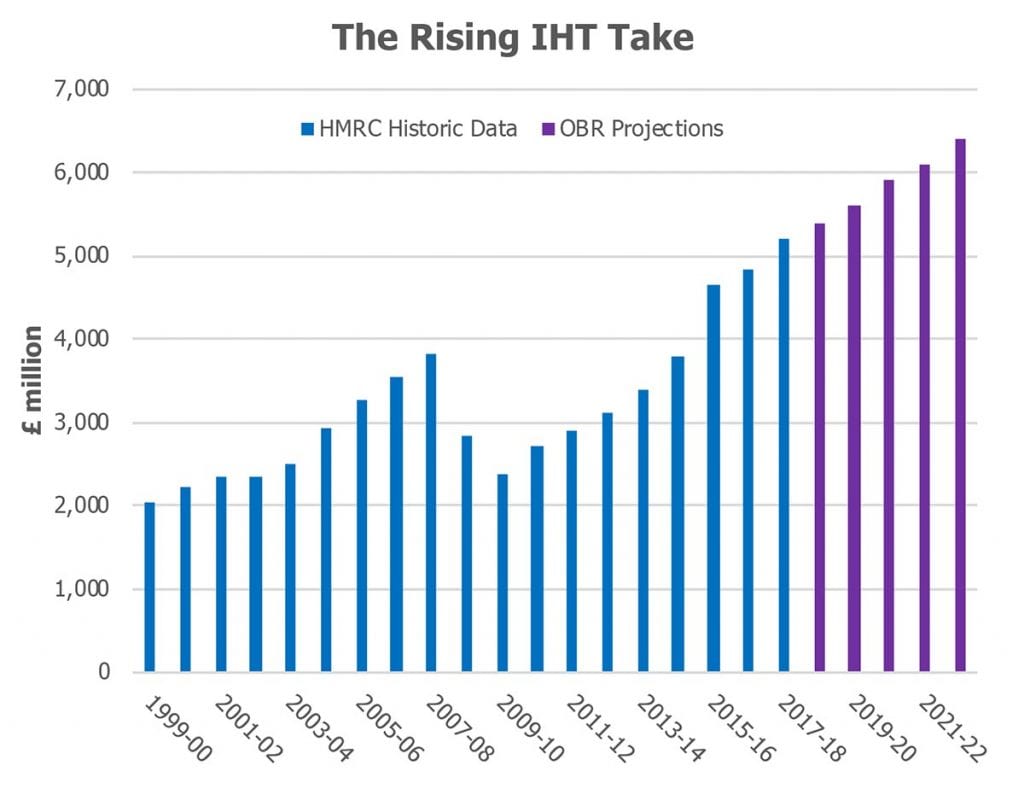

2017/18 produced record inheritance tax (IHT) receipts according to HMRC data published in July.

The latest release of the annual statistics revealed IHT produced £5.228 billion for the Exchequer in 2017/18, an increase of two thirds over just five years. As the graph shows, IHT revenue has been rising rapidly since Treasury receipts hit a low in 2009/10, owing to the impacts of the financial crisis and the introduction of the transferable nil rate band.

The Office for Budget Responsibility (OBR) expects the growth to continue, although the rate of increase will slow for the next few years because of the introduction from April 2017 of the residence nil rate band.

The Office of Tax Simplification (OTS) is currently undertaking a “general simplification review” of IHT. The OTS is focusing on the administrative aspects of IHT, but it is also looking at the “complexities arising from reliefs and their interaction with the wider tax framework”. With the OTS due to report ahead of the Autumn Budget, it is possible changes and/or pre-emptive legislation will be announced then.

It is unlikely reforms will lead to a reduction in the money raised by IHT. It may be the most unloved tax in the UK, but Mr Hammond has to find an extra £20.5 billion a year for the NHS by 2023 and IHT receipts are above £5 billion a year and rising. The politics of any cut would also be difficult to implement.

There is a case for reviewing your inheritance tax planning now, and possibly taking some action ahead of the Budget. Tax simplification can often bring to mind the words of ‘Big Yellow Taxi’ by Joni Mitchell:

Don’t it always seem to go That you don’t know what you’ve

got ‘til it’s gone.

The value of tax reliefs depends on your individual circumstances.

Tax laws can change.

The Financial Conduct Authority does not regulate tax advice.

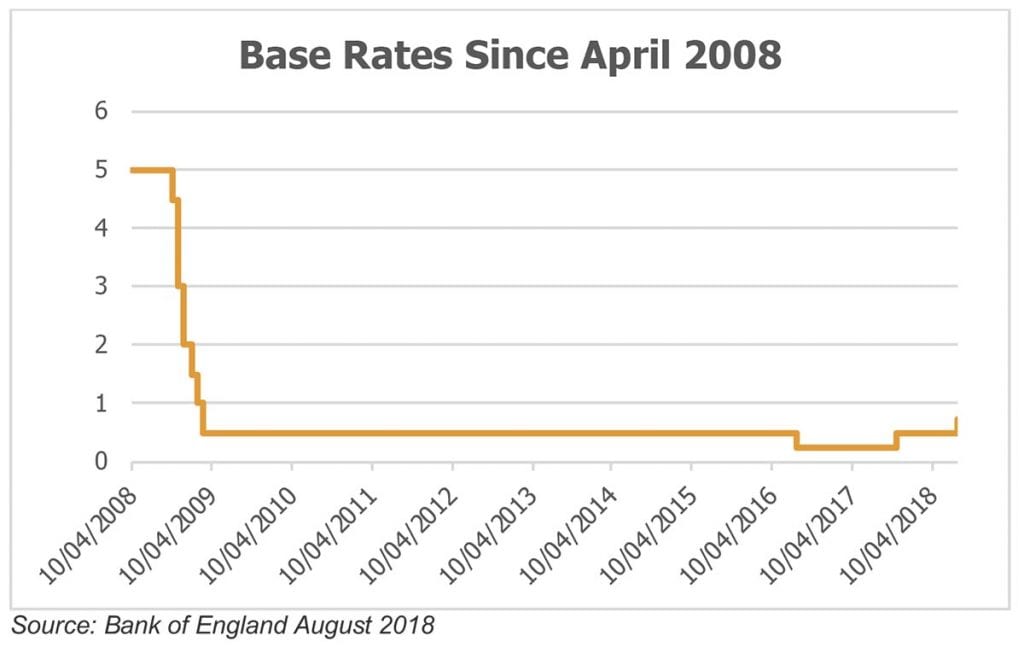

The Bank of England increased the base interest rate in August to 0.75% – the second increase in 12 months.

The Bank’s decision to raise the rate to its highest level in nearly nine and a half years was no great surprise to the investment community. Of more interest to the experts were the comments the Bank offered on the long-term trend of base rates relative to inflation. The Bank gave a theoretical estimate of the base rate needed to maintain inflation and economic growth in a fully functioning economy, rather than another forecast of where rates might be in a year’s time.

The Bank said an interest rate of 0%–1% above the rate of inflation, with a ‘modal rate’ of 0.25%, would achieve this equilibrium. In today’s economic environment, with an inflation target of 2%, this would mean a base rate of around 2.25%. That implies:

The equilibrium rate will be a long time coming – several 0.25% increases would be required and the Bank has repeatedly said any changes will be gradual.

Returns on savings accounts will continue to be poor and often below the rate of inflation, even before the impact of taxes are allowed for.

Persistently low interest rates mean that holding too much money on deposit could damage your long-term financial health. Whilst we all need to put aside reserves for the proverbial rainy day, the UK has moved on from an era when base rates were expected to be a useful margin above inflation.

For an assessment of how much your ready cash reserve should be, and the options for investing any excess, please talk to us.

The value of your investments, and the income from them, can go down as well as up and you may not get back the full amount you invested.

Past performance is not a reliable indicator of future performance.

Investing in shares should be regarded as a long-term investment and should fit in with your overall attitude to risk and financial circumstances.

The rates charged on student loans rose at the start of September.

The revised terms for interest on, and repayment of, student loans were published in August, along with the A level results for the year. From 1 September, the main interest rates for Plan 2 loans, taken out by students and recent graduates in England and Wales, are:

Period

Interest Rate

During study and until the April

after leaving the course.

6.3%

From the April after leaving the course

(maximum 30 years).

On a sliding scale, rising from:

3.3%, where income is £25,725 or less; up to

6.3%, where income is £46,305 or more.

Plan 1 student loans, taken out by students in Scotland and Northern Ireland (and students in England and Wales whose course started before 1 September 2012), carry a 1.75% interest rate.

Both rates represent an increase – 0.2% for Plan 2 and 0.25% for Plan 1. The first was driven by an increase in the RPI for March 2018 against March 2017, and the second by last month’s base rate rise.

The income threshold at which loan repayments start to be made will also rise from 6 April 2019, to £25,725 for Plan 2 RPI-linked loans and £18,935 for the older Plan 1 loans. The repayment level will be held at 9% of the excess income, meaning the cheaper loans will require higher repayments.

Tax implications

The 9% repayment rate has the same effect as an increased tax rate above the threshold. An employed basic rate taxpaying graduate therefore could suffer a marginal ‘tax’ rate of 41% in 2019/20 – 20% income tax + 12% national insurance contributions (NICs) + 9% loan repayment.

Including auto enrolment, the same graduate could also be required to make pension contributions of 4%, net of tax relief, making for total deductions of 45%. As auto enrolment contributions disappear above the upper earnings limit and NICs drop to 2% above the higher rate threshold, the maximum overall rate facing a higher rate taxpaying graduate is 51% (40% income tax + 2% NICs + 9% loan repayment).

The Institute for Fiscal Studies believes that in practice 80% of graduates will never fully repay their loans, as they will have the outstanding amount written off after 30 years (or an earlier death). That makes planning to provide funds for your student child/grandchild to help them avoid having to borrow a potentially unrewarding idea.

A more effective strategy could be to make sure that they have adequate financial resources when they graduate to help them cope with those high effective rates of tax. For help with how that can be arranged, please talk to us now – even if the graduate is still only at primary school, it is never too early to start planning.

The US stock market set a new record for the longest-ever bull market in August.

Wednesday 22 August 2019 saw the S&P 500 drop – by less than 0.1% – after 3,453 days, making it the longest-ever bull run (a period of rising share prices) for the index, which is used by professional investors’ as a yardstick for the US stock market.

The previous record was set between 1990 and 2000, a period that saw the dot-com boom, followed shortly after the start of the new millennium by the tech bust.

The current rally has been helped by a strong performance from technology stocks, notably the ‘FAANGs’ (Facebook, Apple, Amazon, Netflix and Google (now called Alphabet)). It has also been aided by a period of ultra-low interest – the US Federal Reserve’s main rate was set to a historic low in December 2008 and did not rise above 1% until June 2017. In the last year US companies have also benefitted from Donald Trump’s corporate tax cuts, which have boosted earnings figures.

Despite the record performance, this bull market has been labelled as “the most hated of all time”. Throughout, sceptics have viewed the market as trading on borrowed time and reliant on the easy-money policy of the US central bank. How much longer the rally can last remains a hot topic.

While interest rates are now rising the US economy is growing strongly, and that is working its way through to the bottom line of the now more lightly-taxed US companies. Similarly, while the S&P 500 index is regularly reaching new peaks, other measures of valuation show US shares much less highly valued compared to previous market peaks.

Whatever the future holds, the past near nine and a half years have provided a reminder of the wisdom of international diversification of investments.

The value of your investment can go down as well as up and you may not get back the full amount you invested.

Past performance is not a reliable indicator of future performance.

Investing in shares should be regarded as a long-term investment and should fit in with your overall attitude to risk and financial circumstances.